Call Monday-Friday 9am - 6pm Closed Weekends & Bank Holidays

[ Contact Us ]

Need Help? Calling from a mobile please call 0151 647 7556

0800 195 4926Do you have a question? or need help?

Call Monday-Friday 9am - 6pm Closed Weekends & Bank Holidays,

Looking for cover? Click and get a GAP Insurance quote

You can see exactly how this is calculated in our guide to how GAP Insurance claims are calculated

Below are example GAP Insurance prices based on real quotes generated on 6th May 2026. Prices vary depending on the vehicle, cover type and policy term.

| Vehicle Value | GAP Type | 2 Years | 3 Years | 4 Years |

|---|---|---|---|---|

| £14,999 | RTI | £77.89 | £98.97 | £159.98 |

| VRI | £88.98 | £128.96 | £193.94 | |

| £29,999 | RTI | £108.97 | £184.97 | £257.89 |

| VRI | £128.98 | £223.98 | £298.89 | |

| £49,999 | RTI | £138.97 | £223.79 | £268.98 |

| VRI | £158.98 | £259.98 | £318.98 |

Prices shown are inclusive of Insurance Premium Tax. Premiums generated on 6th May 2026 and may change over time.

Please select some policies.

We are here to help! Search our help centre for any questions you may have.

Aequitas Automotive is our parent company.

The telephone number is exactly the same 0800 195 4926

Our company registration number is 7347606.

We have been trading since 2010.

Aequitas Automotive Limited is part of the Aequitas family of companies and is Owned by Aequitas Group Holdings.

Our address is, Aequitas House, 56 Hamilton Square, Birkenhead, Wirral, CH41 5AS.

Our FCA Number is 821163

Our ICO registration number is Z2455374.

Acasta European Insurance Company Limited underwrote all policies purchased from March 2018 until 7th February 2024. Since the 7th of February 2024, Financial & Legal Insurance Company Limited will underwrite all Gap insurance policies while Acasta European Insurance Company continues to underwrite all other policies we provide.

Yes all of our policies are backed by the FSCS.

No providing that you have adjusted the number of years then the price on screen is for the full term of your policy.

No, you can pay using a credit card at no extra charge. You can also pay using American Express at no additional charge.

You can pay for your policy with a credit, debit card or even American Express at no extra charge, PayPal, or Bank transfer. If you would like to pay in monthly instalments, simply call a member of the team on 0800 195 4926 | 0151 647 7556 or use PayPal Pay in 3. ( to find out more please click the Pay in 3 icon above)

You will be asked to give your details including your bank account and sort code. Premium Credit the company that provide the funding will then either write or email to confirm that you are aware of the agreement and then normally 10-14 days later your first deposit instalment will be taken. Your regular monthly payment will then be on the same day of the month that you purchased your policy.

If you pay monthly you will need to pay a small deposit payment. Your first instalment will normally be 10-14 days later and then this will be followed by a further 11 equal instalments. This means that there will be a total of 12 monthly instalments however your cover will continue until the end of your policy.

Some gap insurance policies have a claim limit. A claim limit is the maximum amount that your gap insurance will pay on top of whatever your insurance company offer you in settlement. For vehicles up to £75,000, we do not have one. Your policy will simply pay whatever it needs to. For vehicles over between £75,000 and £100,000 there is a maximum claim limit fo £75,000.

The maximum length of coverage for Gap Insurance is 5 years. For other policies, it is 4 years. Excess insurance is an annual renewable policy.

No, at present, Total Loss policies do not cover motorbikes. Please try our other sister system www.easygap.co.uk

No sorry at present Total Loss policies do not cover motor homes instead, please try www.easygap.co.uk

In an ideal world the policy would be in the name of the person who own's the vehicle and is the principle insurance policy holder. However this is not always possible so we would request that if this is not the case please contact a member of the team on 0800 195 4926 who will be able to advise the best course of action so as to not invalidate your insurance.

Yes, you can cancel at any time; please see our cancellation and cooling off the page in the "Important Information" section.

No problem simply register your policy using the registration number which is currently on your vehicle. When DVLA give you authorisation to use your number plate simply contact us and we can amend your policy completely free of charge.

No problem simply contact a member of the team who will update your policy. This normally takes just a few minutes and is completely free of charge.

If you are putting a private plate on your vehicle simply let us know when DVLA have said it is "ok" to change your number plates. We can amend your policy and issue new documentation. Please note this is a free of charge service.

No. Once you have claimed on your GAP Insurance the policy is spent. If you replace your vehicle with another, then a new policy would be required if you wish to have GAP Insurance cover for that vehicle.

No problem you can put in the registration box 'TBA' and just call the team when you have your registration number or your private plate has been registered with the DVLA and we can update that for you completely free of charge.

The purchase price of your vehicle is the total cash price after any discounts but before any cash deposit or part exchange allowance.

No, on the understanding that you allow us to talk to your insurance company, we will pay the difference between your insurance company's settlement regardless of book or market values.

Yes, you can transfer your policy to your next eligible vehicle completely free of charge. (T&C's Apply)

You must let us know that your vehicle has been written off within 120 days.

As a perk of purchasing a comprehensive motor insurance policy, some providers will offer a 'new for old' term. If you have purchased a brand new vehicle, within the first 12 months of ownership, if the vehicle was declared a total loss, subject to terms and conditions, your own motor insurer would simply replace the vehicle. Therefore, you may not need/want the Gap Insurance in place during the first year and instead may want to delay the start date until the cars first birthday.

This will depend on the purchase price of your vehicle as well as the number of years that you would like to cover. Click for a quote, and our system will automatically generate a price. Or you can call 0800 195 4926, where a team member will be only too happy to help.

Currently, we can not provide total loss cover for vehicles over 3500kg, to be used as a taxi, driving school or other form of hire and reward, racing, rallying, competition, motorbikes or motorhomes. For a full list of eligibility, please see your policy documents. For a quote on Motorbikes, Motorhomes, taxis & Driving School vehicles. Instead please visit our sister system Easygap.co.uk.

No, as the DVLA will automatically refund any unused proportion directly back to you.

You must buy your policy within 180 days of taking delivery (age and mileage conditions apply) or up to 365 days if you have New for Old cover with your own fully comprehensive insurance provider. We would, however, point out that until your policy is live, you leave yourself financially exposed.

Yes providing that your own motor insurance company have said it is a valid claim.

Yes, on the understanding that your motor insurance covers you, you are covered in the UK, Northern Ireland and Scotland, and any other EU member state for up to 90 days in a calendar year.

No your driving history is not taken into consideration.

No, instead, we pay up to £250 towards your motor insurance company excess.

The purchase price is the amount that your garage / dealership have invoiced you for. This is after any discounts but before any cash deposit or part exchange allowance. This does not include any interest.

A deferred policy is a policy where you have elected to set the start date to co-inside with your vehicles first birthday.

Some insurance companies almost as a perk of buying a new vehicle will within the terms of your comprehensive motor insurance policy say that if you buy a new vehicle and your name is first on the V5, if it is written off within the first 12 months, that they will simply go and buy you another.

Hire and reward means that you are paid to use your vehicle to transport people or objects from one place to another.

It means that your own insurance company have looked at the reason as to why your vehicle was declared a total loss and have agreed to settle.

Where your own insurance have decided that the cost of repairing your vehicle is not economically worth while, or it has been stolen and not recovered.

The Financial Conduct Authority. This is the governing body of all financial products in the UK.

The Financial Services Compensation Scheme

The organisation who you can complain to if you are not happy and your complaint has not been resolved.

This is the date that you would like your Total Loss Gap Insurance policy to start.

This is the total cost of your policy.

Insurance Premium Tax (almost like VAT on insurance)

The list price of your vehicle - normally only needed if you are buying your vehicle on a contract or lease hire.

This is the amount of money outstanding on your finance agreement. (this does not include any late payments charges, arrears and regrettably can not refer to personal loans)

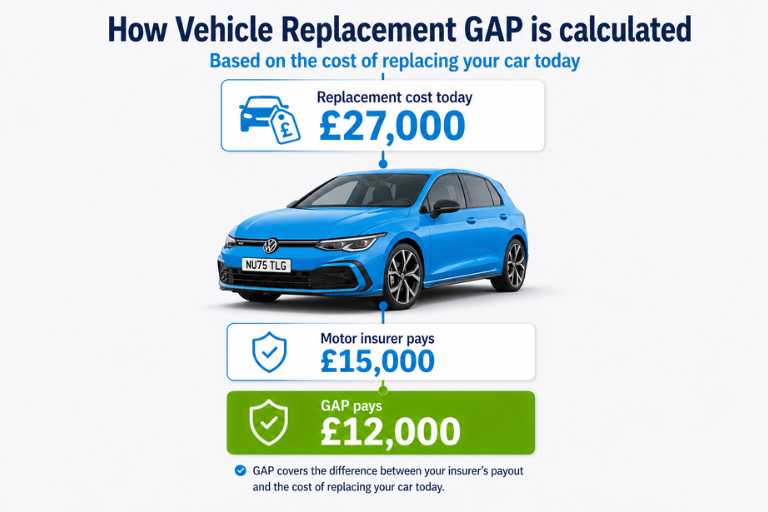

The cost of a Replacement Vehicle, matching the original Vehicle specification or an equivalent superseding model in the event this is no longer available.

This is any shortfall between your part exchange value and the amount outstanding on finance which you have re-financed on top on the purchase price of this vehicle.

This is a list of countries that your gap insurance policy will cover you in. (a full list is available in your policy terms)

This is the company that you are buying your policy from.

This is the organisation who will responsible for settling your claim.

This is the insurance company who back your policy.

This is a vehicle that you have imported yourself from another country.

This is the amount that your own motor insurance company will deduct from your settlement under the terms of your policy. This will include your voluntary and compulsory excess.

A claim where your motor insurance company have investigated and decided that you were attempting to make a claim under false pretences ( dishonest ).

This is the document from DVLA which will show that you are the legal keeper of the vehicle.

This is a number plate which you have purchased to use on a vehicle often called a cherished number plate.

This is a set time during which you can change your mind and cancel your policy and (providing you have not made a claim) and have a full refund.

We will cover named drivers on your motor insurance policy over the age of 18 with a full licence. So, whoever is driving your vehicle when it is written off, as long as your own insurance company are happy to settle, then so are we.

Without seeing your dealership's policy it is impossible to confirm. We can however say that as of yet we have never seen another policy as comprehensive anywhere in the UK, either online or from dealerships.

No, you do not have to buy gap insurance from any one and certainly if you buy a policy from us you have up to 180 days.

No, unfortunately we are not based somewhere exotic. Instead we are based in a Hamilton Square in a beautiful Grade 1 Listed Georgian Town House which was converted to offices some time ago.

Yes and no? There are a million and one ways to write a vehicle off and for your vehicle to be stolen. Rather than list each one and still never cover all of them our policy simply says that you own insurance company must be happy to settle. If they are we simply follow suit. So for example, if someone steals your car your own insurance will settle and will will follow suit. If however you leave the keys in the ignition, door open and someone then steals it? Your own insurance company would not settle and therefore our hands would be tied.

For policies purchased before March 2023 - Spectrum is a specialist claims team that deals with your policy should you ever need to make a claim.

Spectrum are based Sheffield.

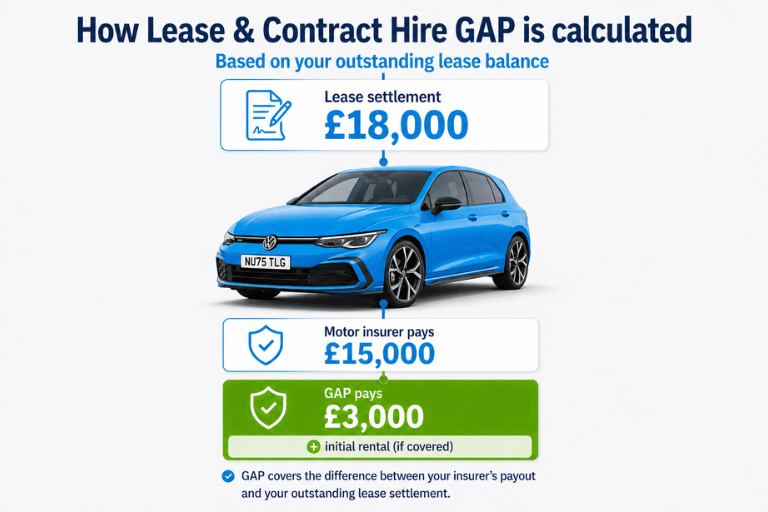

Contract Hire gap insurance is a policy specific to leased and contract-hired vehicles.

Contract Hire gap insurance will pay the difference between your insurance company settlement on the day your vehicle is written off and the amount needed to settle your lease or contract hire agreement. It will not cover any late payment charges or arrears.

Your contract hire gap insurance policy will not cover any late payment charges or arrears on your lease as these would be deducted from any settlement.

Without any form of gap insurance for your contract hire / lease car, if it is written off you could be faced with the fact that you no longer have a vehicle to use and also have to pay any financial shortfall. This is because legally you are responsible for any difference between your motor insurance companies settlement and the amount needed to clear your lease.

A contract hire finance shortfall is the difference between your insurance company's settlement and the amount you need to pay off your lease. This could be made up of several factors. Differences in market value, back rentals, outstanding rentals and your lease company may call it something completely different. No matter what it is called, if you have no outstanding rentals or late payment charges, this is exactly what we clear.

No, our contract hire policies are for private vehicles only and can not cover any hire and reward usage.

No, your alloy wheel insurance policy does not cover theft you would need to claim on your motor insurance policy.

The maximum number of claims during the period of alloy wheel insurance shall not exceed the amount you have chosen. E.g. 2 or 4 claims per year.

Policies purchased after March 2023 have no excess. Polices purchased before then have a £10 excess payable on each claim.

For policies purchased after March 2023, the claims team number is 0345 040 5975. For policies purchased before March 2023, the claims team number is 0114 321 9877

Accidental damage is a sudden and unforeseen event that has resulted in damage to your alloy wheels. e.g. you scraped or kerbed your alloy wheel.

You can purchase Alloy Wheel Insurance for your vehicle, provided it is under 8 years old and the recorded mileage on the vehicle odometer is less than 80,000 miles. For vehicles over 5 years old, we will need to be emailed within 5 working days, clean, dry images of your alloys to show that there is no damage, before we can authorise the policy. The vehicle must have been purchased within the preceding thirty-day period and must have been supplied by a main dealer or VAT-registered garage.

The policy will not cover any vehicle used at anytime in a public service capacity,such as Military,Police or Ambulance vehicles. Vehicles used for hire and reward,courier and delivery services,and short-term self drive hire.Also,vehicles used for the carriage of passengers,including but not limited to private hire and taxi services.Vehicles used for driving instruction in connection with your occupation are also not covered. The policy will not cover any vehicle used at any time for any type of competition usage,be that any form of rallying,racing,any type of track day,off road,speed testing,pace making or reliability trials. The policy will not cover split rim construction,chrome rim,multi-piece or chrome finished alloy wheels. The policy is not renewable but subject to eligibility we may be able to transfer the cover to your newly purchased vehicle. There is an initial thirty day claim waiting period after the start date during which you are not able to process a claim. The policy will not cover any damage which is the result of poor maintenance and neglect.Corrosion of the wheel is not covered.Any previous sub standard previous repair is not covered(unless previously arranged by the Claims Administrator).The policy will not cover manufacturing defects,design faults or any damage resulting in improper cleaning,polishing or adjustment. The policy will not cover any costs to repair the alloy wheel(s) fitted to the insured vehicle that the Claims Administrator does not authorise in advance and provide an authorisation number for. The policy will not cover any costs to repair the alloy wheels(s) where the damage is caused by wear and tear due to age and/or usage.Any damage that occurs when a replacement tyre is fitted,damage that occurs whilst the insured vehicle is driven with an under-inflated tyre or by a road traffic accident involving another vehicle where a motor insurance claim has been made are not covered.The policy does not cover defective,failing or peeling paint or lacquer.The theft of wheel nuts or the insured vehicle itself are also not covered.

Your alloy wheel policy will pay for a cosmetic repair to your alloy wheel. If the wheel is no longer viable (e.g. cracked ), then your wheel would be scrapped, and as a token of goodwill, your policy would pay £150. We know that this will not buy you a new wheel. This is just a goodwill gesture. For a full list of terms and conditions, please visit Our alloy wheel page, where you will be able to see the full policy terms and conditions.

The policy schedule is a document issued to you when you purchase your alloy wheel insurance. It will provide details of the policyholder, the insured vehicle, the length of cover, the policy identification number and the purchase price of the policy.

From March 2018, policies will be underwritten by Acasta European Insurance Company Limited.

Yes, to keep costs to a minimum, we will not honour any claim made within the first 30 days of purchasing your policy unless you have purchased a brand-new car and bought your policy before you have taken delivery.

Yes, you can transfer your alloy wheel policy to your next eligible vehicle.

Yes, you can cancel your alloy wheel policy at any time. If you cancel within the first 30 days, you will be given a full refund, provided you have not attempted to make a claim. After this time, you can cancel and receive a pro-rata refund less a £35.00 fee retained by the underwriter. If, however, you have made a claim, you have had the benefit of the policy and there will be no refund.

You can make two or four claims during any twelve months of the policy term, depending on how many claims you chose when you bought your policy.

For policies purchased after March 2023, there is no excess to pay. For policies purchased before March 2023, there is a £10 excess payable on every claim made during the policy period.

Policies purchased after March 2018 are underwritten by Acasta European Insurance Company Limited.

Accidental damage is a sudden and unforeseen event that has resulted in damage to one or more of your tyres.

The following vehicles are excluded from Tyre Insurance coverage: Taxis, self-drive hire, driving school, service vehicles, e.g. Police, ambulance, etc. Commercial vehicles or vans with a carrying capacity exceeding 1500kg. Any vehicle used in competitions, rallies, pace making or off-road use. Left-hand drive vehicles. Vehicles not listed in Glass's Guide. Any vehicle owned temporarily or otherwise by a motor dealer ,trader or business formed for the purpose of selling or servicing motor vehicles.

Replacing tyres can be extremely expensive. Tyre insurance will pay for the cost of repair or replacement of your tyres which has resulted from damage that has occurred within the geographical limit.

You can make as many claims as you have chosen when you bought your policy within 12 months. You can check how many claims you chose, as this will be shown at the top of your document.

For policies purchased after March 2023, there is no excess. Policies purchased before March 2023 are subject to a £10 excess for each claim.

If your policy was purchased after March 2023, please call 0345 040 5975. If you purchased your policy before then please call 0114 321 9877.

Your policy will cover damage up to 30cm in length and 3mm in depth and the damage can be on two panels. For more information, please see our Scratch and Dent page located in our Additional Policies menu.

The policy is underwritten by Acasta European Insurance Company Ltd

To be eligible for this policy your vehicle must have a standard paint finish which is not self healing, chrome illusion, two tone, matte finish or has been vinyl wrapped.

You can purchase Scratch and Dent Insurance for your vehicle provided it is less than 8 year old and the recorded mileage on the vehicle odometer is less than 80,000 miles. For vehicles over 5 years old, we will need to be emailed within 5 working days, clean, dry images of your vehicles bodywork to show that there is no damage, before we can authorise the policy. The vehicle must have been purchased within the preceding thirty-day period and must have been supplied by a Main Dealer or a VAT-registered garage.

You can claim at any time; however, to keep costs to a minimum, we will not honour any claim made within the first 30 days of purchasing your policy unless you had bought a brand-new car and purchased your policy before you took delivery of your car.

Financial Services Compensation Scheme FSCS for short is an independent body who are there to help protect you if the underwriter is no longer able to pay our claim.

BIBA is the British Insurance Brokers Association and we are proud members.

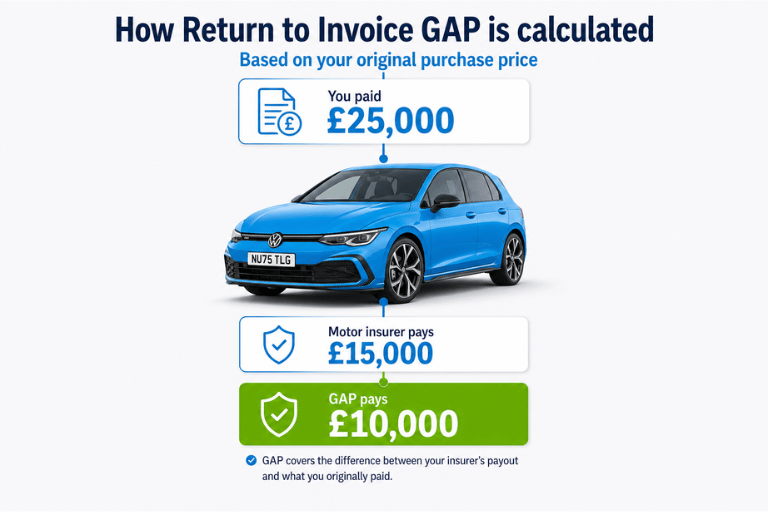

Return to invoice gap insurance means that if your vehicle is written off, your policy will top up your motor insurance company's settlement to either the amount outstanding on finance or the original invoice price you paid, whichever is the higher. From this, you can clear any finance if necessary, and the balance of funds (the difference between the invoice price you paid and the amount outstanding on finance -if applicable) is then yours to spend as you see fit. For more information, please see our Return to Invoice page, which is in the Gap Insurance menu.

Yes providing that your invoice shows the cost for the paint protection then it would be covered in the event of a valid claim.

No we do not cover any late payment charges or arrears. Your claim would be calculated exactly the same however any arrears or late payment charges would be deducted from your settlement.

Yes all of our policies will include an element of insurance premium tax which will be passed on to HMRC. However please don't worry the price you are shown is already inclusive of IPT.

At present (Jan 2024) the current rate of IPT (Insurance Premium Tax) charged on independently purchased gap insurance / supplementary insurance is 12%.

Yes, providing that you have set the start date to the date you wish the policy to start, your cover will start immediately. (Please remember that if you have a deferred policy, this will not start until the date you have chosen, and we can not cover accidents or thefts that have already happened.)

No sorry we can not cover any vehicles which have already been written off.

Total Loss Gap is pleased to confirm that we have been recognised as the 'Best Buy' for GAP Insurance in the UK by motoring giant Auto Express.

Auto Express undertook an independent survey of various Gap Insurance providers in the UK. They took a standard quote from a franchised primary dealer for a £32,270 vehicle and obtained a quote for three year Gap cover for £449.  This quote was then compared against many online providers for alternative quotations.

This quote was then compared against many online providers for alternative quotations.

Auto Express highlighted the ease at which a quote can be obtained from the Total Loss Gap website.

It confirmed the premium found at Total Loss Gap was 59% cheaper than the motor dealer at £185.28

Total Loss Gap was the ONLY provider to be given a full 5 out of 5-star rating.

Total Loss Gap was also awarded the 'Best Buy' for Gap Insurance in the UK for 2021.

Auto Express also commented that Total Loss was the only provider they found to allow deferred start dates. This would allow a later start date if the motor insurers' replacement cover covered the car in year one.

In awarding the Best Buy to Total Loss Gap, Auto Express concluded that we were 'Clear, honest and good value.'

A spokesperson for Total Loss Gap said 'We are honoured to be the only Gap Insurance provider to get a 5 Star award and the only Gap provider to get the 'Best Buy' recommendation from such as name as Auto Express."

"At Total Loss Gap, we always strive to provide our customers with the best 'value' with the products we provide. Value can be found in the service we provide, the features you get, and the premium price you pay. It is great to see that an industry giant agrees with us too."

The Auto Express Gap Insurance review can be found in the current magazine and can be found on the Auto Express website also. (CLICK HERE to see)